Goldman Sachs – November Market Pulse

Summary

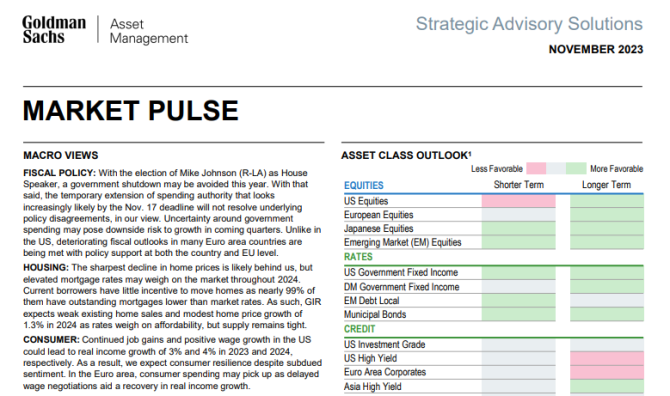

The November Market Pulse by Goldman Sachs provides an overview of various market trends and predictions.

In terms of fiscal policy, the election of Mike Johnson as House Speaker may help avoid a government shutdown. However, the temporary extension of spending authority is unlikely to resolve underlying policy disagreements, which could pose downside risks to economic growth. Unlike in the US, many Euro area countries are addressing deteriorating fiscal outlooks with policy support at both the national and EU levels. In the housing market, the sharpest decline in home prices is likely behind us. However, elevated mortgage rates may continue to weigh on the market throughout 2024. Current borrowers have little incentive to move homes as most of them have mortgages lower than market rates. As a result, weak existing home sales and modest home price growth are expected. Consumer resilience is anticipated despite subdued sentiment due to continued job gains and positive wage growth in the US. The Euro area may see an increase in consumer spending as delayed wage negotiations contribute to a recovery in real income growth. Higher interest rates have raised concerns for corporate expenses, but a major uptick in defaults is not expected. Many companies that took advantage of low rates in the past decade have also earned positive net interest income, strengthening their credit. US Treasury yields have reached their highest levels since 2007, driven by strong growth momentum and increased government bond issuance. However, it is predicted that yields are nearing their peak and may edge lower in the coming months due to weaker fourth-quarter growth and tighter financial conditions. The ongoing conflict in the Middle East is putting upward pressure on oil prices, outweighing any softening caused by high US oil production. The forecast for Brent oil prices remains at $100 per barrel, with a potential upside risk if the situation in the Middle East leads to a reduction in Iranian supply. Aggregate earnings for S&P 500 companies have exceeded consensus expectations. In 2024, the focus may shift towards growth investments in the AI space and supportive fiscal policies, potentially providing longer-term payoffs. In Chinese equities, three sectors - battery, EVs, and renewable energy - have emerged as new sources of growth. However, overall GDP growth in China is expected to slow due to downturns in the property and real estate sectors and weakening consumption. Exposure to secular growth trends and strong company fundamentals is advised given the challenging macro conditions.

Region:

Published:

Author(s):

Language:

Tech drivers:

Found an inaccuracy in the description? Let us know 🙌

Latest Viewed Reports